The Hard Reality of Selling a Fire-Damaged Home in Arizona

Selling a fire-damaged house in Arizona is often far more difficult and emotional than most homeowners expect. A house fire doesn’t just damage walls and floors. It dismantles your sense of normal. One moment, you have a home; the next, you’re standing in the driveway wondering what to do next about your family, your finances, and a property you may not be able to live in or sell.

If you’re reading this, you’re probably in that moment right now. And you need real information on how to sell your fire-damaged house, not empty reassurances.

If your home has been damaged by fire, you’re probably staring down a mountain of questions:

- Can I even afford to repair this?

- Will my insurance cover enough?

- Is it worth fixing, or should I just sell?

- Who would even buy a fire-damaged house?

- What happens if I can’t afford the repairs and can’t pay the mortgage?

Arizona homeowners face this reality more often than many people realize. In 2025 alone, Arizona recorded 1,608 wildfires that burned 331,629 acres statewide, according to the Arizona Department of Forestry and Fire Management’s annual wildfire data. But wildfire damage is only part of the picture. Residential fires caused by electrical faults, kitchen accidents, HVAC failures, and aging infrastructure happen year-round across Phoenix, Scottsdale, Mesa, and communities throughout the Valley, leaving many homeowners facing difficult decisions about what to do with a damaged property next.

This guide answers all of those questions. We’ll walk you through how to assess the damage honestly, what your insurance will and won’t cover, the true cost of repairs, your selling options, and what to do if repairs simply aren’t financially possible.

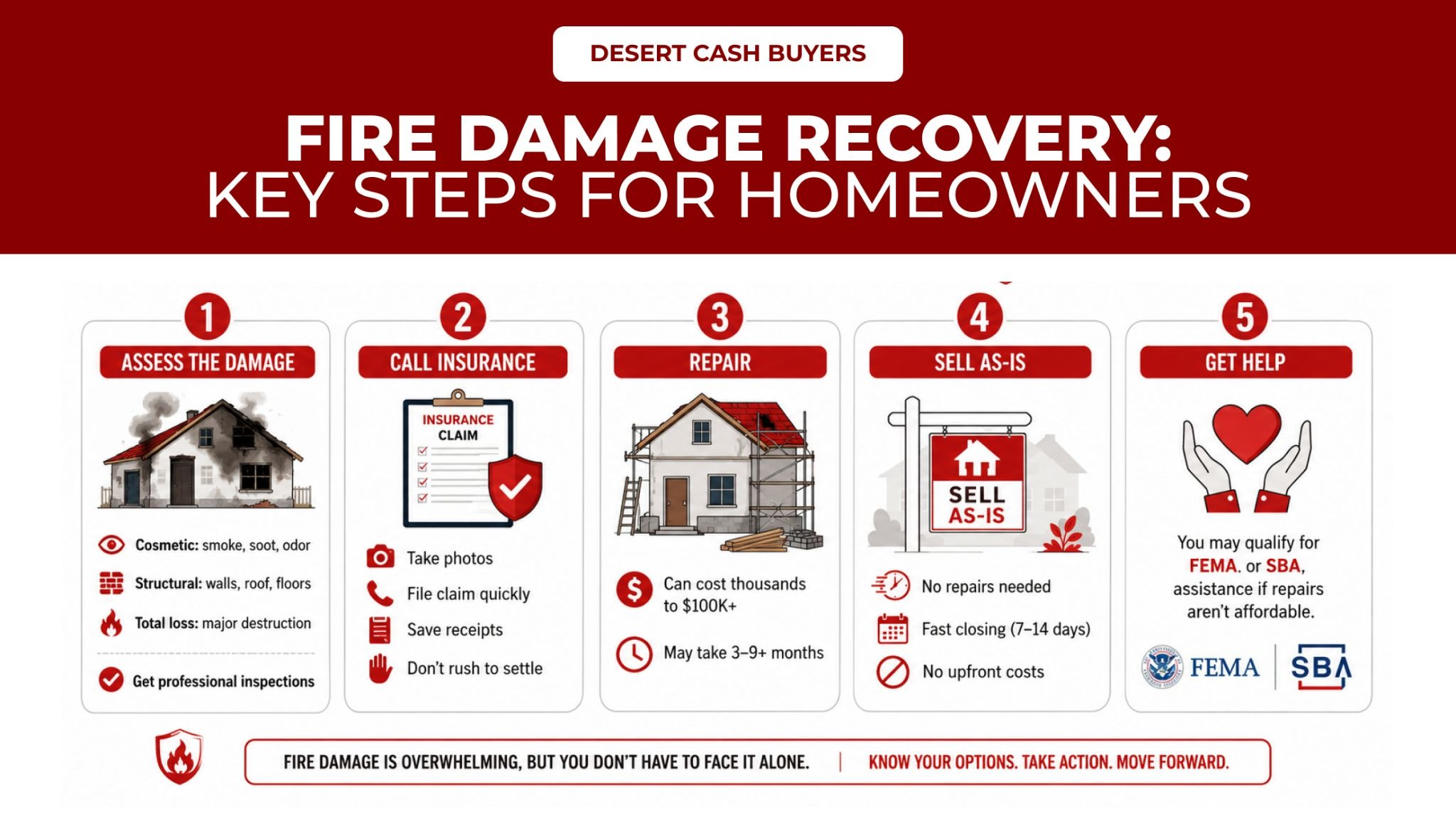

Step 1: Assess the Damage. What Are You Actually Dealing With?

Assessing fire damage starts with understanding exactly what the fire impacted, because the severity of the damage will shape every decision that follows. Fire damage falls into three categories, and which category your property falls into changes everything.

Cosmetic Damage Only

The fire was contained quickly, and structural elements are intact—walls, roof framing, and foundation. What you’re dealing with is smoke residue, soot staining, odor, and possibly water damage from the firefighting effort. Cosmetic damage is fixable, but don’t underestimate it. Smoke infiltrates HVAC systems, embeds in drywall, and can hide inside walls in ways that aren’t visible until a professional inspection.

Structural Damage

This is where most house fires land. The fire was hot enough or burned long enough to compromise load-bearing elements—wall studs, roof trusses, and floor joists. Structural damage is significantly more expensive and requires permits, inspections, and licensed contractors. It also takes months.

Total Loss or Near-Total Loss

When a fire burns unchecked—a wildfire, a gas leak ignition, an unoccupied home—the structure may be unsalvageable. In these cases, the cost to rebuild often exceeds the home’s post-repair market value, making the repair path economically irrational regardless of what you want to do.

The Damage Assessment Checklist

Walk through your property only after fire officials have cleared it as safe. Use this checklist:

Structural integrity:

□ Are walls, load-bearing beams, or roof trusses visibly charred, warped, or collapsed?

□ Are any floors buckled, soft, or compromised?

□ Is the foundation cracked or shifted?

□ Has the roof been penetrated or partially collapsed?

Systems damage:

□ Is the electrical panel damaged, or was the fire electrical in origin?

□ Are gas lines exposed, melted, or compromised?

□ Has the HVAC system been exposed to smoke or heat?

□ Is plumbing intact, or has PEX/copper been damaged?

Smoke and water:

□ Is smoke odor present throughout the home, not just near the fire’s origin?

□ Are walls and ceilings stained with soot beyond the immediate fire area?

□ Is there visible water damage from firefighting or any early signs of mold?

Always get at least two independent assessments: a licensed structural engineer ($350–$900) and a certified fire damage restoration contractor, before accepting any single estimate. Their reports also become important documentation when dealing with your insurance company.

One more practical note: do not attempt to board up, clean, or remove debris from the property on your own before your insurance adjuster has visited. Disturbing the damage scene before it has been documented can complicate your claim or give the insurer grounds to dispute your payout. If the property is an active safety hazard, contact your insurer first and ask for emergency stabilization authorization. Many policies cover emergency board-up and tarping costs, but only if you go through the right channels before the work is done.

Step 2: Understand Your Insurance Options

Your homeowner’s insurance is your first resource, but it comes with limitations that many Arizona homeowners don’t discover until they’re already in the middle of a claim.

What Standard Policies Typically Cover

Most standard homeowner policies cover fire damage under the dwelling coverage (Coverage A) portion. This typically includes structural repairs, system replacement (electrical, HVAC, plumbing), temporary living expenses while your home is repaired, and personal property up to policy limits.

What They Often Don’t Cover, Or Don’t Cover Enough

• Underinsurance: If your home’s rebuild cost has risen since you took out the policy, and in Arizona’s post-pandemic construction market, it likely has, your coverage limit may fall short of actual repair costs.

• Code upgrades: Repairs on older homes often require bringing systems up to current Arizona building codes. Many policies exclude these upgrade costs.

• Mold remediation: If firefighting water causes mold before the home is dried out, some policies exclude this.

• Personal property sub-limits: These can be lower than homeowners expect.

What to Do Immediately After the Fire

1. Contact your insurer within 24–48 hours. Most policies have prompt-reporting requirements.

2. Document everything before anything is moved or cleaned. Photos and video of every room, every surface, every damaged item.

3. Request your full policy in writing: declarations page, Coverage A limits, ALE provisions, and exclusions.

4. Keep every receipt for temporary housing, clothing, and emergency expenses, these are typically reimbursable.

5. Do not sign any releases from your insurance company until you understand the full scope of damage and costs. Early settlement offers are often insufficient.

One thing many Arizona homeowners don’t realize: your first settlement offer from the insurance company is rarely the final one. Insurers typically open with an estimate based on their adjuster’s walkthrough, which may undervalue the scope of the damage, especially hidden smoke infiltration, code upgrade requirements, and contents losses.

You have the right to dispute the offer, request a re-inspection, or hire a licensed public adjuster to represent your interests independently. A public adjuster typically charges 10–15% of the final settlement but can meaningfully increase the payout on complex fire damage claims. Before signing any settlement agreement, get your independent contractor estimates in hand, so you know whether the offer actually covers what the repair will cost.

Step 3: The Repair Path: Full Cost Breakdown

If insurance covers a significant portion of your costs and the home has strong post-repair value, repair may make sense. Here is what you are actually looking at.

Average Fire Damage Repair Costs (2025–2026 Data)

| Damage Type | Cost Range |

| Smoke damage restoration | $200 – $1,200 per room |

| Soot removal (professional) | $2,000 – $6,000 |

| Water damage from firefighting | $1,000 – $6,000 |

| Air duct / HVAC cleaning | $250 – $500 |

| Thermal fogging (odor removal) | $200 – $600 |

| Ozone treatment (odor removal) | $400 – $800 |

| Structural repairs (per room) | $15,000 – $25,000 |

| Full home restoration (moderate damage) | $3,098 – $52,031 |

| Extensive structural damage | Up to $180,000+ |

The national average for fire damage restoration is $27,564, according to HomeAdvisor’s 2025 data. That figure covers the full spectrum from minor smoke-only cleanup to moderate structural damage. Homes with extensive structural damage: compromised framing, collapsed ceilings, and fire-damaged foundations, can push well beyond $100,000 and, in severe cases, approach $180,000 or more.

The Repair Timeline: 3 to 9+ Months

• Weeks 1–2: Insurance adjuster visits, damage assessment, contractor estimates

• Weeks 3–6: Debris removal, structural shoring, temporary weatherproofing

• Months 2–4: Structural rebuilding, rough systems work (electrical, plumbing, HVAC)

• Months 4–7: Drywall, insulation, flooring, cabinetry reinstallation

• Months 7–9+: Final finishes, inspections, permits closed

During all of this, you are paying for temporary housing and carrying a mortgage on a home you cannot live in.

The Repair Path: Honest Pros and Cons

Pros: Potentially recovers full market value. Insurance may cover a significant portion. You retain ownership and equity.

Cons: Out-of-pocket costs are often substantial even with insurance. The timeline is long and unpredictable in Arizona’s busy construction market. No guarantee the repaired home sells for more than the total investment when carrying costs are included.

The repair path makes sense when insurance covers 70% or more of repair costs, the post-repair value significantly exceeds your total investment, and you have the financial cushion to manage the gap and monthly payments during a 6–12 month rebuild.

Step 4: The As-Is Cash Sale Path: Sell Without Making a Single Repair

For many Arizona homeowners, selling a fire-damaged house as-is to a cash buyer is the faster, lower-stress, and more financially rational path. Here is what that actually looks like.

Why Traditional Buyers and Lenders Reject Fire-Damaged Homes

This is the reality most homeowners don’t know until they try to list:

• Conventional lenders won’t finance fire-damaged homes. Fannie Mae and Freddie Mac require homes to be in livable condition at purchase. FHA, VA, and conventional loan buyers are eliminated from your buyer pool.

• Traditional buyers back out after inspection. Even motivated buyers typically have inspection contingencies. Once an inspector documents structural issues or smoke infiltration in the HVAC, most buyers walk, often after you’ve been under contract for weeks.

• Insurability problems. Many insurers won’t write a new policy on a fire-damaged home until it is fully restored, making it nearly impossible for a financed buyer to close.

Cash buyers operate outside all of these constraints. They fund with their own capital, buy in any condition, and don’t require lender approval.

What You’ll Need to Have Ready

Gathering these documents speeds up the process with any cash buyer:

□ Current mortgage statement (showing payoff amount)

□ Homeowner’s insurance policy and claim documentation

□ Insurance adjuster’s damage report, if available

□ Any contractor estimates already received

□ Title or deed information

□ HOA documentation if applicable

□ Fire department incident report

Repair vs. As-Is Cash Sale: The Decision Matrix

| Factor | Repair Path | As-Is Cash Sale |

| Timeline to close | 6–12+ months | 7–14 days |

| Upfront cost required | $0–$100,000+ out of pocket | $0 |

| Certainty of outcome | Moderate, delays common | High, offer locked in |

| Final sale price | Full market value (post-repair) | Below full market; may net similarly after carrying costs |

| Mortgage carrying costs | 6–12 months of payments on an unlivable home | Eliminated immediately |

| Stress level | High | Low |

| Best for | Strong insurance, high ARV, financial cushion | Unaffordable repairs, urgent timeline, certainty needed |

Note on carrying costs: When you factor in 6–12 months of mortgage payments, insurance, and utilities on an unlivable home during a repair project, the net proceeds from the repair-then-sell path are often closer to a cash offer than homeowners initially expect.

If the fire has caused you to fall behind on mortgage payments and foreclosure is becoming a concern, read our guide on how to stop foreclosure. Selling to a cash buyer is often the fastest path to resolving both issues at once.

Step 5: What to Do If You Can’t Afford Repairs

If you are underinsured or the repair costs vastly exceed what insurance will cover, you are not without options.

Federal Assistance Programs

If your fire is part of a federally declared disaster, which is more common after major wildfire events, FEMA may provide financial assistance for uninsured or underinsured losses.

FEMA assistance may include:

- Financial help for home repair or replacement costs not covered by insurance

- Assistance for temporary housing, including rental assistance or hotel reimbursement if your home is unlivable

- Support for medical expenses, personal property replacement, transportation, and other disaster-related needs

- A one-time Serious Needs Assistance payment of $790 per household for immediate necessities such as food, water, baby formula, fuel, medication, or transportation

Apply as soon as a disaster declaration is announced through DisasterAssistance.gov. Filing deadlines are strict and vary by event.

SBA Disaster Loans

You do not need to own a business to qualify for an SBA disaster loan after a fire.

Current SBA disaster loan limits include:

- Up to $500,000 for homeowners to repair or replace a primary residence damaged in a declared disaster

- Up to $100,000 for renters or homeowners to replace personal property such as furniture, appliances, clothing, or vehicles

- Low interest rates with repayment terms up to 30 years, depending on eligibility

- Additional funding for mitigation improvements, with borrowers potentially eligible for up to 20% above verified physical damage costs to help reduce future disaster risk

Apply through SBA.gov/disaster or call 800-659-2955.

Since FEMA’s 2024 policy updates, homeowners no longer need to wait for an SBA denial before being considered for many FEMA assistance programs, so it often makes sense to apply to both at the same time.

When Assistance Still Isn’t Enough

Government programs help, but they don’t always bridge the full gap, especially for homeowners facing both repair costs and monthly mortgage payments on a home they can’t live in. In these situations, selling the fire-damaged home as-is to a cash buyer often makes the most financial sense:

• You stop the bleeding immediately, no more mortgage payments on an unlivable home.

• You get certainty, a locked-in offer, a closing date you control, and funds at closing.

• You can move on once temporary housing ends, finances stabilize, and you reset.

Why Cash Buyers Are the Most Realistic Option for Fire-Damaged Homes

Cash buyers are often the most realistic option for fire-damaged homes because they can purchase properties as-is without requiring repairs, financing approval, or lender-required inspections.

• No financing contingencies. Cash buyers don’t need a mortgage, so lender restrictions on property condition don’t apply. The deal doesn’t fall apart because an appraiser flags structural damage.

• No requirement to repair, clean, or stage. You leave what you want and take what you want. The buyer handles everything after closing.

• Speed. Desert Cash Buyers can provide an offer in 15 minutes or less and close in as little as 3 days. Compare that to 6–12 months for a repair-then-list approach.

• Certainty. Cash offers don’t fall through due to financing. Once you accept, the timeline is in your hands.

• Any condition. Whether your home has cosmetic smoke damage or is a near-total loss, cash buyers work with the full spectrum of fire damage.

What Determines the Cash Offer on a Fire-Damaged Home?

The cash offer on a fire-damaged home is typically based on the home’s after-repair value, the estimated cost to restore it, and the level of risk the buyer takes on during the project.

Many homeowners going through a fire for the first time wonder how a buyer can put a number on a property that has been damaged. In reality, the process is often more straightforward than expected. Most cash buyers use the same core framework to evaluate the property and calculate a fair as-is offer.

1. After-Repair Value (ARV)

After-repair value is what the home could reasonably sell for on the open market once all repairs are completed and the property is fully restored.

This number is usually based on recent comparable sales in your neighborhood, including homes with similar square footage, condition, lot size, and location. Buyers rely on local market data rather than broad ZIP code averages to estimate this value accurately.

2. Estimated Repair Costs

The next factor is the projected cost to repair the fire damage and bring the home back to livable condition.

For a fire-damaged property, this may include:

- structural framing repairs

- roof replacement

- smoke and soot remediation

- HVAC cleaning or replacement

- electrical rewiring

- plumbing repairs

- drywall and insulation replacement

- permit costs and code upgrades required by the city

This part of the calculation often has the biggest effect on the final offer because repair costs can vary significantly depending on the severity of the damage.

3. Buyer Risk and Project Margin

Cash buyers also account for the risk involved in taking on the project.

Fire-damaged homes can come with hidden issues that are not always visible during the first walkthrough. Delays with permits, contractor scheduling, material costs, insurance complications, or additional structural problems discovered during demolition can all increase the total investment required.

Because of that, buyers build in a margin that allows the project to remain financially viable while taking on those uncertainties.

The Basic Formula

Most cash offers follow a simple formula:

After-Repair Value − Estimated Repair Costs − Buyer Margin = Cash Offer

For example, if a fire-damaged home in Phoenix could be worth $400,000 after full restoration and needs $120,000 in repairs, the as-is cash offer may fall somewhere around $230,000 to $260,000, depending on the condition of the property, neighborhood demand, and the scope of work involved.

For many homeowners, the value is not just the offer amount itself. A cash sale often means selling the home as-is, avoiding repair expenses, skipping agent commissions, and closing in a matter of days instead of waiting months for a traditional buyer.

How Desert Cash Buyers Handles Fire-Damaged Homes

Desert Cash Buyers has been serving Arizona homeowners for over 10 years and has purchased more than 1,000 homes across Scottsdale, Phoenix, Chandler, Mesa, Tempe, Cave Creek, and Gilbert. The company is BBB-accredited and has a 4.9/5 rating from thousands of verified sellers.

Here is exactly how the process works:

- Schedule a visit in person or by phone. Tell us about your property and describe the fire damage. No obligations, no commitments. We explore all options with you.

- Get a fair cash offer in 15 minutes or less. We assess the property and come back to you with a no-obligation cash offer. No repairs needed, no commissions, no hidden fees.

- Accept and get paid on your timeline. If you accept, we close on your schedule; we don’t rush you to move out. A licensed and insured title company handles all paperwork.

That is it. No showings, no staging, no back-and-forth with lenders. You take what you want from the home and leave the rest.

We’ve worked with homeowners facing every kind of fire damage situation: wildfire damage, kitchen fires, electrical fires, total losses, across every price point. Our goal is a fair offer and a smooth transaction every time.

Learn more about selling your fire-damaged house for cash or explore our as-is selling process

Frequently Asked Questions about Selling a Fire-Damaged House in Arizona

Can I sell a fire-damaged house in Arizona without making any repairs?

Yes. Cash buyers purchase fire-damaged homes in any condition: no repairs, cleaning, or staging required. Traditional buyers using mortgage financing cannot purchase fire-damaged homes due to lender restrictions, but cash transactions have no such limitations.

How much less will I get compared to the home’s pre-fire value?

It depends on the severity of the damage and your market. A cash offer reflects the as-is land and structure value, minus the buyer’s estimated repair costs. In many cases, especially when you factor in 6–12 months of carrying costs during a repair and relist, homeowners net comparable amounts to what they would have after going the repair route.

Do I need to disclose the fire damage when selling?

Yes. Arizona requires sellers to disclose material facts, and fire damage is a material fact. Attempting to conceal it creates serious legal liability. The good news is that cash buyers expect fire damage; disclosure doesn’t kill a cash deal.

What if I still have a mortgage on my fire-damaged home?

You can still sell. The cash buyer purchases the home, the mortgage is paid off at closing from the proceeds, and you receive any remaining equity. If the home is underwater, the damage makes the property worth less than the mortgage, there are options worth discussing directly. Reach out to Desert Cash Buyers and explain your situation.

What if my home is a total loss? Can it still be sold?

Yes. Even a complete loss has land value, and cash buyers purchase lots and burned-out properties. The offer will reflect land value minus any demolition costs.

How long does it take from first contact to closing?

With Desert Cash Buyers, you can have a cash offer in 15 minutes or less and close in as little as 3 days. If you need more time to sort out insurance, secure temporary housing, or gather paperwork, we close on your schedule.

What if my insurance claim is still open? Can I still sell?

Yes, but it requires coordination. In some cases, insurance proceeds can be structured at closing. In others, you complete the claim first and then sell. The right approach depends on your policy. Call us at 503-770-0145, and we can help you work through the timing.

What are my legal responsibilities for a fire-damaged home I’m not living in?

As the owner of record, you remain legally responsible for the property even if it’s uninhabited and uninhabitable. That means maintaining the property to avoid code violations, securing it against unauthorized entry, and carrying liability insurance even while it sits vacant. Many standard homeowner policies have vacancy clauses; if the home sits empty for more than 30–60 days, coverage may be reduced or voided. Arizona municipalities can also issue fines for unsecured or blighted properties. This is one more reason a prolonged repair timeline carries hidden costs beyond just the mortgage payment: you’re also managing ongoing liability on a property you can’t use.

Is there any cost to getting a cash offer?

No cost, no obligation, no pressure. No commissions and no hidden fees. Getting an offer from Desert Cash Buyers is simply information; it helps you understand your options before making any decision.

You Have More Options Than You Think When Selling a Fire-Damaged House in Arizona

Owning a fire-damaged home in Arizona feels like being stuck. The home is unlivable, the costs feel impossible, and the traditional selling process seems blocked at every turn.

But you’re not stuck. The path forward depends on your specific situation:

- If insurance covers most of the repairs, and the numbers work, repair, restore, and sell through traditional channels.

- If repairs are partially covered but you have the cash cushion, evaluate the total cost, including carrying costs, before committing to the repair path.

- If repairs are unaffordable, you’re falling behind on the mortgage, or you simply want to move on, a cash sale is often the fastest and most financially sound decision.

Desert Cash Buyers purchases fire-damaged homes throughout the Phoenix metro and greater Arizona. We move fast, we’re transparent about our process and offers, and we’ve helped hundreds of Arizona homeowners navigate exactly the situation you’re in right now.

Ready to understand what your fire-damaged home is worth?

Get Your Free Cash Offer — No Repairs Required

No obligation. No pressure. Just clear information so you can make the right decision for your situation.